How Leopold Aschenbrenner Turned an AI Manifesto Into a $13.7 Billion Bet

From OpenAI researcher to one of Wall Street’s most aggressive AI infrastructure investors and the bottlenecks he believes will shape the next decade.

For the past year, I’ve been obsessed with a question that most investors still underestimate:

What happens when AI demand becomes too large for the physical world supporting it?

As an engineer working around large-scale data systems and someone using AI tools every single day in my workflow, I’ve been watching the acceleration firsthand. Models are improving rapidly. AI usage is exploding across industries. Compute demand keeps climbing. But beneath all the excitement around Nvidia, OpenAI, and frontier models, another story has quietly started unfolding: the infrastructure underneath AI is beginning to crack under the pressure.

Power shortages. Data-center constraints. GPU scarcity. Grid limitations. Cooling bottlenecks.

That’s why the rise of Leopold Aschenbrenner caught my attention early.

While most of Wall Street was focused on the obvious AI winners, Aschenbrenner was building a completely different thesis: the biggest opportunities may come from the bottlenecks created by AI itself.

And unlike most theorists, he backed that conviction with billions.

Leopold Aschenbrenner: The Engineer Who Saw the Bottleneck First

At just 24 years old, Leopold Aschenbrenner has become one of the most closely watched figures in AI investing.

Not because he built another AI startup.

But because he identified something most investors were still ignoring: the physical infrastructure limits of AI.

Born in Germany, Aschenbrenner moved to the United States as a teenager, graduated as valedictorian from Columbia University at 19, researched economic growth at Oxford, and eventually landed at OpenAI during one of the most important technological shifts in modern history.

At OpenAI, Aschenbrenner worked on the Superalignment team focused on ensuring increasingly powerful AI systems behave safely. But his time there ended abruptly in 2024 following disagreements around security and internal information sharing.

What happened next changed the trajectory of his career.

Two months after his firing, he published a 165-page essay titled “Situational Awareness: The Decade Ahead.” In it, he made a sweeping, unfashionable argument: Artificial General Intelligence (AGI) was not a distant sci-fi concept but a plausible reality by 2027. The world, he argued, was utterly unprepared for the geopolitical, economic, and infrastructure consequences.

The essay went viral in Silicon Valley circles. Within months, Aschenbrenner had raised $225 million in seed capital from Stripe co-founders Patrick and John Collison, former GitHub CEO Nat Friedman, and AI investor Daniel Gross. He reportedly invested nearly his entire net worth into the fund alongside them. Thus was born Situational Awareness LP.

By the February 2026 13F filing, Situational Awareness LP disclosed $5.52 billion in U.S. equity exposure. By the May 2026 filing (covering Q1 2026), that number had surged to $13.68 billion across 42 positions.

The Framework Behind the $13.7 Billion Bet

1. Thesis-First Investing, Not Stock Screener Investing

Aschenbrenner did not find Bloom Energy by screening for cheap valuation multiples or momentum breakouts.

He started with a worldview.

If AGI arrives by 2027, compute demand explodes.

If compute demand explodes, power demand explodes with it.

And if power demand explodes, the existing grid cannot support it fast enough.

Every investment became a logical bottleneck inside that chain.

This is the reverse of how most hedge funds operate.

Typical managers ask:

“What looks cheap?”

Aschenbrenner asked:

“What becomes essential in a world that is changing faster than markets expect?”

2. Going Upstream from the Obvious Trade

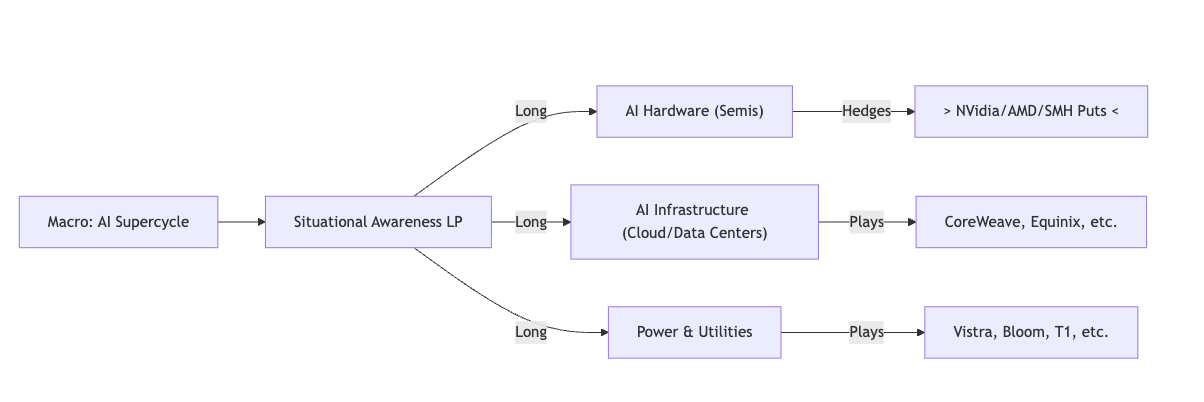

The answer was power plants, optical networking, memory storage, GPU cloud operators, and data-center real estate.

He skipped the chip layer almost entirely and went directly after the infrastructure stack supporting it.

3. Extreme Concentration

The fund never held more than 24 to 42 positions at any time. As of Q1 2026, the top 10 holdings represented over 72% of the portfolio. This is not diversification. It is high-conviction concentration backed by a single, falsifiable thesis. In a world where most fund managers spread risk across 200+ names, Aschenbrenner’s approach is closer to a venture capital bet expressed through public equities.

4. The Key Holdings

Bloom Energy: Solving the Power Bottleneck

The flagship bet. Bloom makes solid-oxide fuel cells that generate electricity on-site for data centers, bypassing a power grid that has a 5+ year interconnection waitlist. A Bloom installation delivers power in roughly 90 days. Revenue grew 34% in 2025, with 40% projected for 2026, and a $20 billion order backlog. Aschenbrenner bought in the mid-$20s. The stock ran substantially.

Bitcoin Miners Turned AI Operators (Core Scientific, Iren, Riot, Hive Digital):

This was his most creative insight. Bitcoin miners sit on pre-connected power infrastructure high-density power sites, land, and grid access that AI companies desperately need and cannot build fast enough. Core Scientific alone announced plans to convert its Pecos facility into a 1.5-gigawatt AI data center campus. Aschenbrenner bought these companies not because he was bullish on Bitcoin but because he was bullish on AI's power demand. His stake in Core Scientific crossed 9.4% of the company.

SanDisk: Betting on AI Memory Demand

AI data centers need memory and storage at massive scale. The more inference runs, the more data needs to be stored and retrieved fast. SanDisk became a pure-play bet on AI storage demand.

Intel Call Options (exited, replaced by puts):

This was one of his earliest and most contrarian trades. Everyone had written off Intel as a business in managed decline. Aschenbrenner bought call options betting that U.S. government CHIPS Act funding would keep Intel’s foundries strategically alive. When the U.S. government took a stake, the options went deep in the money. By Q1 2026, he had rotated the Intel position into puts profiting from the upside, then shorting the same name as chip multiples reached frothy levels.

5. The Barbell Strategy: Aggressive Longs, Massive Shorts

The Q1 2026 13F revealed a sophisticated dual-sided bet. On one side: $5.2 billion in concentrated long positions on energy infrastructure, GPU cloud, Bitcoin miners, and storage. On the other side: $8.46 billion in put options against semiconductor companies and chip ETFs including $2.04 billion on the VanEck Semiconductor ETF, $1.57 billion on Nvidia, $1.07 billion on Oracle, and $1.01 billion on Broadcom.

The logic was simple: AI demand is real, the infrastructure buildout is real, but semiconductor valuations may have run ahead of what long-term returns can justify.

Positioning for the Next Phase of the AI Buildout

The expansion of Situational Awareness from $5.5 billion to $13.7 billion in disclosed exposure within a single quarter suggests Aschenbrenner believes the easy money phase may be over, but the structural thesis is still in its early innings.

The portfolio has not been sold down into strength.

It has been expanded, rotated, and reinforced.

Recent filings and public comments suggest Situational Awareness is doubling down on AI infrastructure and energy, with significant downside hedges. Its Q1 2026 13F (filed May 18, 2026) is revealing:

AI Infrastructure & Cloud: SA has added to and maintained stakes in firms enabling data-center scale. For example, it increased holdings in CoreWeave and Applied Digital. The fund also built a 3.6% position in solar/battery firm T1 Energy (10M shares, ~$44M) in Q1, betting on data-center power. Other new or growing long stakes include CleanSpark, Lumen Technologies, reflecting an emphasis on energy supply for AI.

Semiconductors (Selective Bullish + Hedges): SA still holds core semiconductor plays (e.g. Nvidia, AMD, TSMC in equity or options), but its stance is nuanced. As of Q1, the fund purchased massive index puts on SMH ($2.0B) and single-stock puts on NVDA ($1.57B), Broadcom ($1.01B), AMD ($0.97B), Micron ($0.58B), ASML ($0.49B), Intel ($0.00, position closed). This indicates caution on outright stock exposure. Concurrently it opened new calls on Micron ($422M) and Sandisk ($389M). In summary, SA appears long-term bullish on chips but hedged short-term, protecting against volatility while keeping upside optionality.

Energy & Utilities: The fund continues its theme of “power behind AI.” Top disclosed power/utility holdings (Q1 2026) include Vistra Corp (VST), which was a major position since mid-2025, and EQT Corp (EQT), acquired via options. SA’s Q1 filings also show positions in EEFT (data-center REIT) and others. The sizable Bloom Energy stake (even after trimming ~9% from Q4) suggests ongoing interest in fuel-cell power. And as mentioned above T1 Energy

Macro View: Publicly, Aschenbrenner’s views remain consistent: he warns that AGI could arrive sooner than market expects, making “AI” the dominant economic theme. He has not signaled major shifts away from AI, so we expect continued focus on that theme. Given the hedges placed, the fund may be cautious on near-term interest rates or funding issues (though Aschenbrenner has not explicitly commented on macro policy).

What makes Aschenbrenner’s framework especially interesting is that he does not view this as a single trade.

He views it as a sequence.

First came compute.

Then power.

Then utilities and energy infrastructure.

Eventually, potentially even macro trades tied to interest rates, government borrowing, and capital scarcity created by a massive global AI infrastructure buildout.

In his framework, the AI boom is not just a software cycle. It is an industrial cycle.

Wall Street Is Quietly Converging on the Same Trade

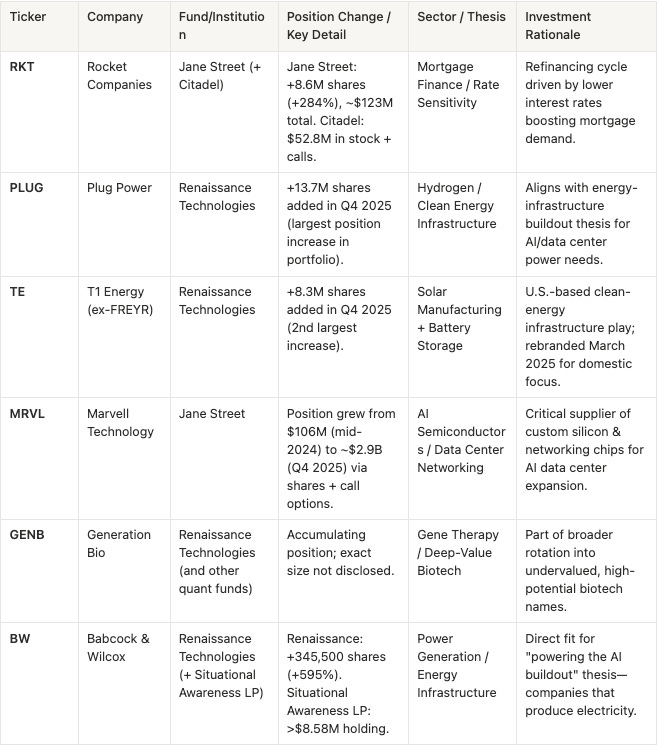

Aschenbrenner is not the only institution betting on this infrastructure theme. The Q4 2025 and Q1 2026 13F filings from the world’s most sophisticated quantitative and multistrategy funds reveal a striking pattern: Jane Street, Renaissance Technologies, and Citadel Advisors have all been rotating capital into the same energy, infrastructure, and deep-value names that align with Aschenbrenner’s thesis though through very different execution styles.

Theme 1: Energy Infrastructure:

The clearest hedge fund convergence is happening around energy infrastructure. Renaissance Technologies made Plug Power its largest position increase in Q4 2025, adding 13.7 million shares, while also adding 8.3 million shares of T1 Energy. Even Babcock & Wilcox, a legacy power-generation company, saw accumulation from both Renaissance and Situational Awareness LP. The message is becoming increasingly clear: as AI compute scales, electricity availability may become one of the market’s most important bottlenecks.

Theme 2: AI Data Center Infrastructure

Wall Street is also rotating toward the infrastructure layer powering AI data centers. Jane Street built a massive position in Marvell Technology, growing its exposure from roughly $106 million in mid-2024 to over $2.4 billion by Q4 2025 through shares and call options. At the same time, companies like Nebius and Applied Digital are attracting growing institutional interest as investors look for less crowded ways to participate in AI capacity expansion beyond the obvious semiconductor trade.

Theme 3: Deep Value / Physical Economy Rotation

Interestingly, the positioning is now expanding beyond traditional AI names. Jane Street increased its Rocket Companies position by 284% in Q1 2026, bringing total exposure to roughly $123 million, while Citadel built a separate $52.8 million position. Renaissance Technologies has also accumulated deep-value biotech names like Generation Bio. Different firms. Different models. But increasingly, many appear to be converging on the same idea: the next phase of the AI cycle may be driven as much by physical infrastructure and capital flows as by software itself.

The Bottom Line: The Signal Beneath the AI Boom

What makes Leopold Aschenbrenner interesting is not just the speed of his rise.

It’s the framework behind it.

He did not build Situational Awareness by chasing quarterly momentum or reacting to headlines. He started with a much bigger assumption:

If AGI arrives sooner than markets expect, the world may experience an infrastructure shock unlike anything the technology sector has faced before.

Power is constrained.

Compute is constrained.

Time is constrained.

The companies solving those constraints may become some of the most important businesses of the next decade.

And increasingly, Wall Street appears to be arriving at the same conclusion from very different directions.

What stands out most to me as an engineer is that many of these bottlenecks are no longer theoretical. AI progress is already beginning to collide with real-world limits around electricity, deployment speed, cooling systems, networking, and physical infrastructure scaling.

In Aschenbrenner’s framework, the AI boom is not just a software cycle.

It is an industrial cycle.

And if that thesis is correct, the market may still be underestimating how large this infrastructure buildout could ultimately become.

As Aschenbrenner wrote in the final pages of his manifesto:

“If we are right about the next few years, it is going to be the most important decade in human history.”

Situational Awareness is betting $13.7 billion that the signal is real.

Thanks for reading DeepSignal. We appreciate you being here, and we hope this helped you spot the signal before the broader market catches up and find strong returns from the shifts that matter most. As always, do your own due diligence and size positions according to your risk tolerance and time horizon. If this deep dive was useful, consider subscribing and share your thoughts in the comments.